The Ultimate Guide to Citi Banking Tiers (2026): Benefits, Perks & Who Each Tier Is For

Confused about Citi’s banking levels? From $500 to $10M+, this 2026 guide breaks down Citi Priority, Citigold, CPC, and Private Bank, plus business account insights and hidden perks..

If you've ever wondered how far your money can go with Citi, from a few hundred dollars to $10 million, this breakdown is for you. Whether you're starting out solo, managing a small team, or running a family office, Citi has tiers to match your financial footprint. Many of them come with fee waivers, credits, and lifestyle perks that aren't obvious at first glance.

This guide isn't just about numbers; it's about what kind of customer each tier is built for and whether it's worth your money, attention, and time.

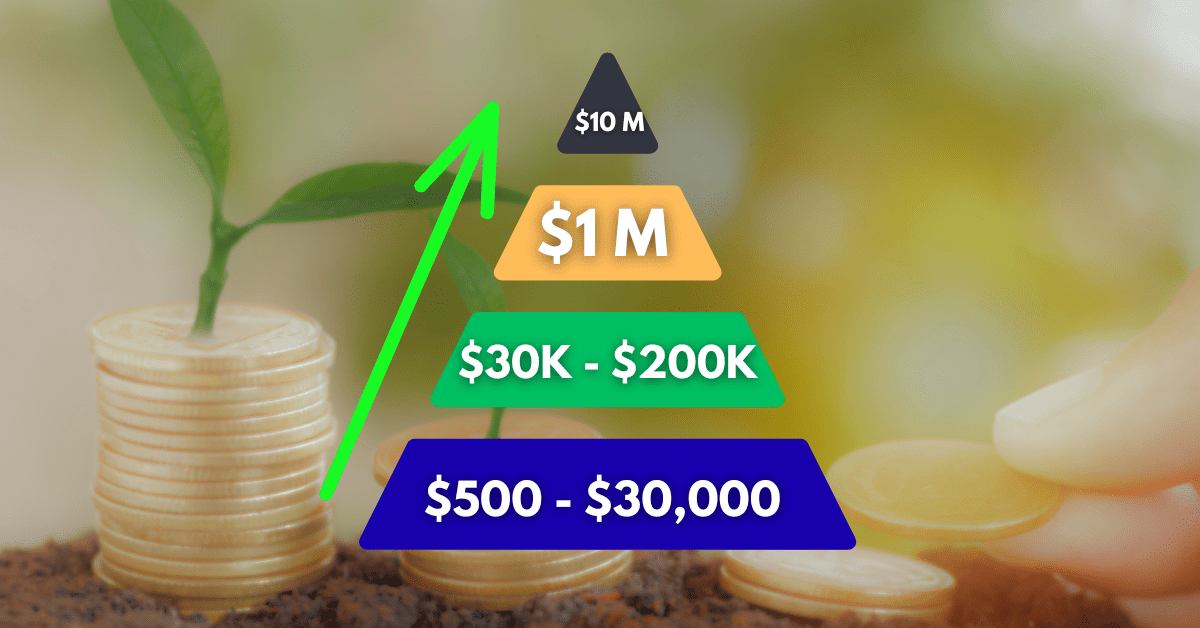

Level 1: Everyday Banking ($0–$29,999)

Who it’s for: Students, freelancers, or anyone new to Citi with basic banking needs.

At this level, you’re not in a formal "relationship tier." You get bare-bones banking and not much else.

Sebby's Take: If you're in this bracket, Citi isn’t your best option. Competitor banks, such as SoFi and Capital One 360, or fintech options, offer no-fee checking with more modern apps and early-access to paychecks. Check out more banking options here.

Level 2: Citi Priority ($30,000–$199,999)

Who it’s for: Individuals starting to build long-term savings, consolidating their finances, or managing joint goals; whether you're a young professional, a couple, or someone moving beyond entry-level banking.

This is Citi’s “starter” relationship tier. You’ve crossed the $30K Combined Average Monthly Balance (CAMB) line, and the bank starts treating you like a client, not just an account number.

Key Perks:

- No account fees on checking/savings

- Waived fees for money orders, official checks, stop payments

- Non-Citi ATM fee waived (but no owner fee reimbursement)

- 3% foreign transaction fee still applies

How CAMB works: Citi adds up your average balances from deposit accounts, IRAs, CDs, and Citi brokerage. You can co-own accounts or link immediate family members in the same household.

Sebby's Take: Priority is good for removing banking friction, but doesn't move the needle on rewards or travel perks. If you’re here for international perks or credit card strategy, you’ll want to level up.

Level 3: Citigold® ($200,000–$999,999)

Who it’s for: HENRYs (High Earners, Not Rich Yet), small-business owners, or investors with six-figure portfolios.

This is where Citi gets competitive.

Why it matters:

- $200/year in automatic statement credits for popular subscriptions (Amazon Prime, Spotify, TSA PreCheck, etc.)

- Global ATM fee reimbursements, including third-party machines

- No FX fees on debit-card purchases or ATM withdrawals

- Free wires (domestic and international)

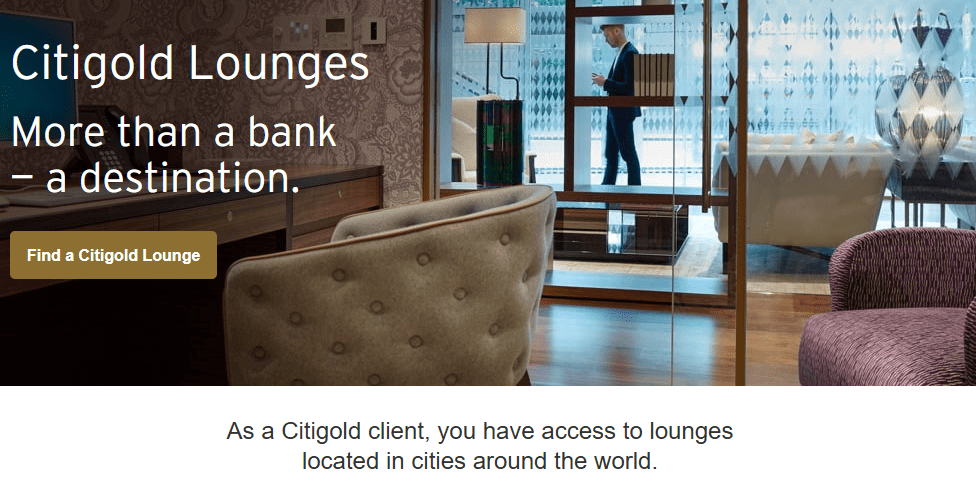

- Citigold Lounges in global hubs (NYC, SF, London, HK, Singapore)

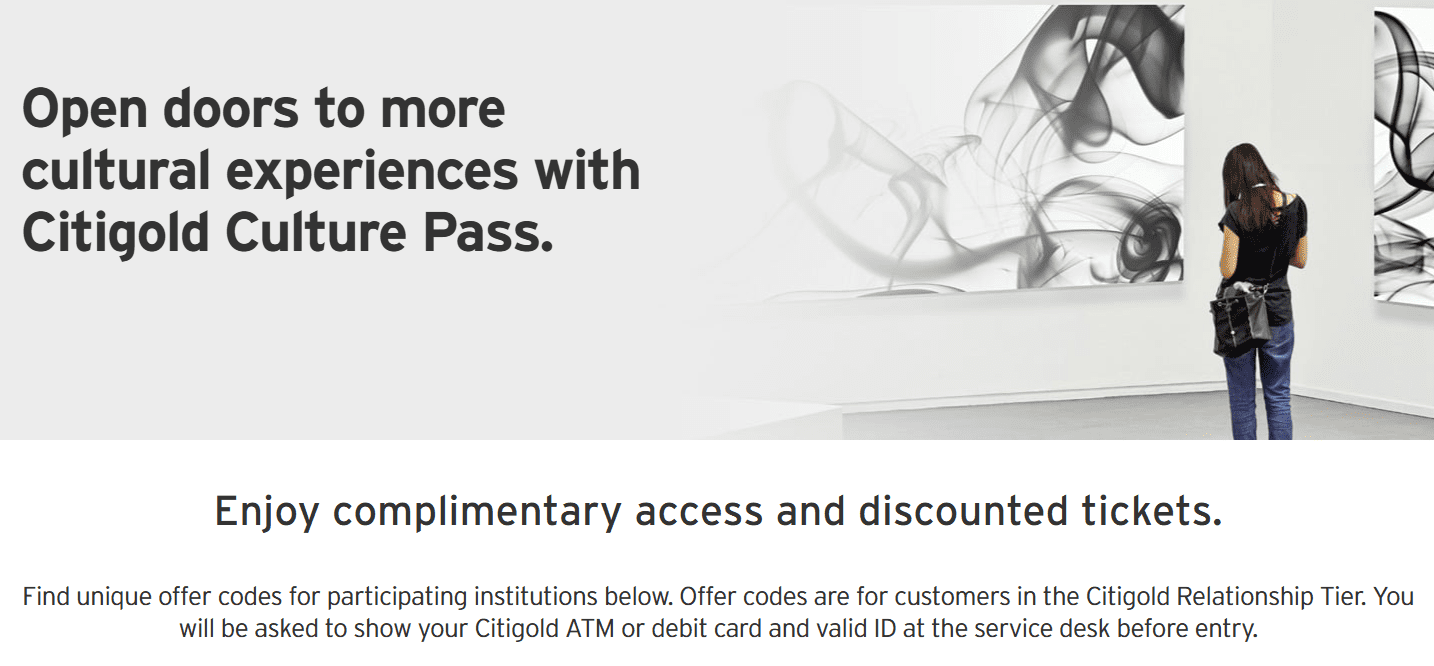

- Complimentary museum access in NYC (MoMA, Guggenheim)

- Free Citi Bike membership (NYC)

Credit Card Boost:

- $145 credit toward Citi Strata Elite, AA Executive, or legacy Citi Prestige annual fee

- These credits stack, so if you hold 2+ cards, that’s real value.

Sebby's Take: Citigold is the sweet spot. If you already hold brokerage or retirement assets, consolidating at Citi unlocks travel-grade perks without needing a travel card. It's the quiet MVP tier.

Level 4: Citigold Private Client ($1,000,000+)

Who it’s for: High-net-worth individuals, real estate investors, or small family offices who prefer simplicity over complexity.

You’re not quite at family-office levels yet, but you want white-glove service, meaningful perks, and direct access.

Upgrades over Citigold:

- $400 annual subscription rebate

- $595 full rebate first year on Citi Strata Elite or AA Exec credit cards

- Higher withdrawal, POS, and deposit limits

- Mastercard Travel & Lifestyle Services:

- 4,000+ luxury hotels with upgrades, breakfast, and credits

- 24/7 concierge

- Airport fast-track (15% off), ResortPass rebate, and Priceless Golf experiences

Sebby's Take: For clients already banking here, CPC feels seamless. But if you're eligible and haven’t switched, this is when you should start making Citi work for you, especially if you’re sitting on liquid investable assets or rolling over from another firm.

Level 5: Citi Private Bank ($10,000,000+)

Who it’s for: Founders, C-suite execs, investors, or multi-generational wealth holders. This is Citi’s ultra-high-net-worth platform.

You gain access to:

- Art-backed lending, aircraft & yacht financing

- Direct capital markets access (block trades, IPO allocations)

- Global credit/mortgage in multiple currencies

- Family Office advisory (governance, structure, generational transfer)

- Curated networking and lifestyle access via Citi Latitude

Event perks:

- Access to Art Basel & Frieze VIP days

- Private dinners in NYC/LA

- Cambridge & Singularity University residencies for heirs

Sebby's Take: If you’ve got the assets, Citi’s global footprint is a huge edge. Private Bank isn’t flashy, it’s functional leverage for complex lives.

Bonus: Citi Business Accounts (Simple Math)

Who it’s for: Small businesses and startups with consistent cash flow.

Sebby's Take: Citi business checking is for operational scale, not perks. It’s ideal if you need treasury features, not credit card synergies. If you're looking for rewards, consider Chase Ink or any of these business credit cards instead.

Final Thoughts: Who Wins with Citi?

Citi banking is quietly powerful, especially if you’re consolidating funds, managing global travel, or leveraging tier-based card benefits. Don’t leave perks on the table.

Frequently Asked Questions (FAQ)

What is CAMB, and how is it calculated?

CAMB stands for Combined Average Monthly Balance. Citi calculates it by averaging your daily balances across eligible Citi consumer deposit accounts and Citi Personal Wealth Management investment accounts. This includes checking, savings, CDs, IRAs, and brokerage accounts you own or co-own.

What happens if my balance dips below the tier minimum?

Citi gives you a 3-month grace period. If your CAMB stays below the required threshold for three consecutive months, your relationship tier will automatically be downgraded at the end of the third month.

Can I regain a tier after losing it?

Yes. You can requalify by maintaining the required CAMB for three full consecutive calendar months. Alternatively, you can enroll in Tier Acceleration, which may restore your tier status in as little as one month if your balance meets the end-of-month threshold.

Are the subscription rebates monthly or annual?

They are annual caps, not monthly. Citigold offers up to $200/year, and Citigold Private Client offers up to $400/year. Once you hit the cap, no more credits will post until the calendar resets.

Do I get multiple credits if I have multiple Citi credit cards?

Yes. The Banking Relationship Annual Credit (e.g., $145/year) applies per eligible card, such as the Citi Strata Elite, Citi AAdvantage Executive, or legacy Prestige card. If you hold all three, you could receive up to $435/year in combined credits.

Do business accounts get relationship-tier perks or credit card discounts?

No. Citi's business checking tiers are separate from the personal banking pyramid and don't provide credit card fee rebates or debit card travel perks.

Can I access Citi lounges with Citigold?

Yes. Citigold and CPC clients can use Citigold Lounges globally. These are not airport lounges but urban client centers in cities like NYC, London, Hong Kong, and San Francisco.

Does Mastercard Travel & Lifestyle Services come with Citigold?

No. It is exclusive to Citigold Private Client debit cards (World Elite Mastercard Debit). It includes hotel upgrades, late checkout, concierge service, and curated travel perks.

Is the Citi Private Bank invite-only?

Not formally, but entry typically starts at $10 million+ in net worth or investable assets. Relationship managers vet potential clients and may accept lower thresholds depending on business fit.

The information related to the Citi bank accounts has been collected by AskSebby.com and has not been reviewed or provided by the issuer or provider of this product or service.

Editorial Note: Opinions expressed here are the author's alone, not those of any bank, credit card issuer, airlines or hotel chain, vendors or companies, and have not been reviewed, approved, or otherwise endorsed by any of these entities.

In this article

- Level 1: Everyday Banking ($0–$29,999)

- Level 2: Citi Priority ($30,000–$199,999)

- Level 3: Citigold® ($200,000–$999,999)

- Level 4: Citigold Private Client ($1,000,000+)

- Level 5: Citi Private Bank ($10,000,000+)

- Bonus: Citi Business Accounts (Simple Math)

- Final Thoughts: Who Wins with Citi?

- YouTube Video

- Frequently Asked Questions (FAQ)